Markets were mixed after a late week rally.

The reaction to the Jobs Report was negative initially, but equities continued with the move higher that started on Wednesday. Softer wages and above-consensus unemployment rate in the report stroke a dovish tone with the market that higher interest rates for longer could be overblown. The futures on the Fed Funds Rate moved higher on Friday to an 86% probability of no rate hike in November from 72% on Thursday. In addition, the probability of no rate hike in December, the last Fed meeting for the year, remain at 57%.

This week could change things depending upon the inflation results released this week.

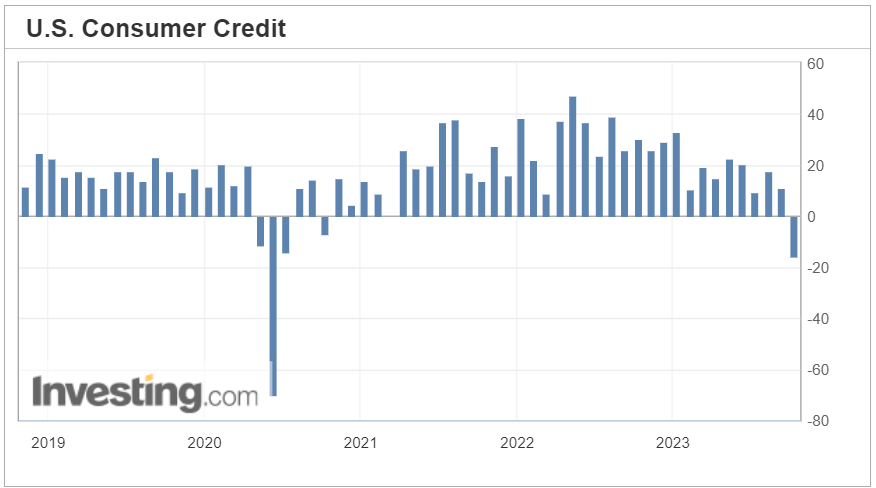

The consensus is that both CPI & PPI decreased in September. More good news on the economic front this past week showed that Job Openings jumped in August after dipping for 4 consecutive months. Both initial and continuing claims dipped last week, and remain at 7-month lows. Factory Orders also jumped in August, but this stands in stark contrast to Consumer Credit, which plummeted in August. If that becomes a trend, it would indicate a weary consumer. Futures overnight have shifted lower as news broke this weekend that groups of Hamas militants attacked Israeli towns along the Gaza border. Oil is trading higher as a result and markets are likely to be choppy this week.

Disclosures

The information contained herein is for informational purposes only and is developed from sources believed to be providing accurate information. The opinions expressed are those of the author, are for general information, and should not be considered a solicitation for the purchase or sale of any security. The decision to review or consider the purchase or sell of any security should not be undertaken without consideration of your personal financial information, investment objectives and risk tolerance with your financial professional.

Forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

Any market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. The S&P 500 Composite Index is an unmanaged group of securities that are considered to be representative of the stock market in general.

Past Performance does not guarantee future results.

Comentarios